Sino-Russian cooperation in the Arctic: options for joint development of rare earth metals

- 1 — Ph.D., Dr.Sci. Head of Department Empress Catherine II Saint Petersburg Mining University ▪ Orcid ▪ Elibrary ▪ Scopus ▪ ResearcherID

- 2 — Postgraduate Student Empress Catherine II Saint Petersburg Mining University ▪ Orcid ▪ Elibrary ▪ Scopus ▪ ResearcherID

- 3 — Ph.D. Associate Professor Taiyuan University of Technology ▪ Orcid ▪ Scopus

Abstract

The rare earth metals (REM) industry plays an important role in the modern global economy due to the extensive use of these elements in high-technology sectors. Russia possesses substantial REM reserves, giving the country a major competitive advantage: a strong mineral resource base capable of meeting growing demand in both domestic and global markets, where China remains the dominant player. China accounts for more than 70 % of global REM production, while Russia’s share does not exceed 1 %. In recent years, countries worldwide have paid increasing attention to the REM supply chain, intensifying international competition in this sector. In this context, the development of Sino-Russian cooperation represents a key factor in strengthening the two countries’ positions in the global market and should be based on collaboration in strategically significant areas for both sides. The purpose of this study is to explore options for implementing a Sino-Russian partnership in strategic sectors, using the REM industry as a case study. The Russian Arctic, where REM deposits unique in terms of reserves and concentrations of valuable components are concentrated, is considered a potential site for the implementation of technological cooperation. The study is based on a critical analysis of Russia’s key REM deposits, with particular attention to Arctic sites, as well as a comparative analysis of the Russian and Chinese consumer markets and forecasts of their development. These analyses form the basis for proposed options for technological cooperation between the two countries. The findings indicate that the most promising form of Sino-Russian partnership is a consortium model, similar to joint projects such as Yamal LNG and Power of Siberia. This format enables Russia to attract investment and technologies, while allowing China to secure access to new sources of raw materials and strengthen its presence in the Arctic.

None

Introduction

Today, rare earth metals (REM) are regarded as critically important materials and strategic resources for modern industry. They are widely used in electronics and mechanical engineering, energy, metallurgy, the production of advanced transport technologies, catalysts, the defense industry, and other sectors [1-3]. Globally, demand for these elements has been growing rapidly, driven by the development of new technologies, artificial intelligence, autonomous robotics, and related fields. In Russia, annual REM consumption amounts to approximately 1.1-1.2 thousand t 1. The key consumers include petrochemicals and oil refining, metallurgy, and the nuclear industry [4]. At the same time, more than 40 % of global REM consumption is concentrated in the production of magnetic materials, which are subsequently used, for example, in wind turbines. As a result, the expansion of green energy in the context of decarbonization and the global energy transition, alongside the growth of other high-technology sectors, has led to an almost twofold increase in global REM demand over the past decade [5]. Currently, China alone consumes more than 170,000 t of REM annually. As for the growth potential of the Russian REM market, the key medium-term driver is the development of new high-technology industries, including renewable energy, electric vehicle manufacturing, aircraft production, etc. [6]. In China, in addition to green energy and advanced transport technologies, the most promi-sing areas for REM demand growth include robotics, electronics, the production of inverter air conditioners, energy-efficient elevators, and other applications2.

Russia possesses one of the strongest competitive advantages in the global REM market, namely substantial reserves estimated at approximately 10 million t in categories A, B, and C1, and more than 30 million t in category C2. More than two-thirds of these reserves are concentrated in deposits located in the Russian Arctic, primarily in the Murmansk Region and the Sakha Republic (Yakutia). In terms of total reserves, Russia ranks after China, the current leader with approximately 44 million t, as well as Vietnam (22 million t) and Brazil (21 million t), where industrial processing facilities are absent3; however, favorable geological assessments show that it may overtake the aforementioned countries in the future. Overall, about 60 % of global REM reserves outside China account for only 30 % of global production, indicating a low level of resource development4. At present, a full value chain for high-technology products based on REM exists only in China. The country leads not only in reserves, but also in extraction, processing, separation, the production of metals and alloys, and the manufacture of final products. By contrast, the United States, Australia, Myanmar, Vietnam, and other countries have production capacities and commercial development at only certain stages of the value chain. However, China’s leadership comes with a number of inherent challenges related to resource base development. Scientific research in recent years has focused on addressing issues such as resource depletion and intensified production, which requires the development of new, more technologically complex deposits. The imbalance in the distribution of heavy and light rare earth elements, the structural deficit of heavy elements accompanied by an excess of light elements, and the environmental consequences necessitate the development of environmentally friendly mining operations, land reclamation practices, and waste recycling methods [7-9].

In Russia, the rare earth supply chain is limited to ore extraction and the production of rare earth metal concentrates, which are subsequently exported. REM consumed domestically are, in turn, largely imported from China5. This contradiction, combined with Russia’s substantial resource endowment, raises concerns regarding the country’s technological sovereignty, considering that governments worldwide have paid increased attention to REM supply chains since 2023. Amid intensifying international competition, REM have gained growing recognition as critical materials for the aerospace, defense, electric vehicles, and other sectors. Western countries, particularly the United States, have significantly intensified their focus on REM production cycles by introducing policy measures and legislation aimed at securing domestic supply, while simultaneously expanding their global influence. In this context, the strengthening of Sino-Russian relations plays a crucial role in enhancing the competitive positions of both countries on the global stage, with the Arctic serving as a connecting platform, partly due to the increasing interest in the region from other nations [10, 11].

Ongoing geopolitical shifts are reshaping traditional trade routes and necessitating the search for new avenues of cooperation. Accordingly, a strategic partnership between Russia and China may represent a response to the challenges associated with diversifying supply chains and identifying new markets [12]. For Russia, the tightening of Western sanctions underscores the need to strengthen ties with new partners, while for China, the introduction of new tariffs by the U.S. presidential administration amid the trade war has imposed additional economic conditions. Cooperation between the two countries should therefore focus on strategically important sectors of the economy and be based on mutually beneficial terms. By strengthening their positions through joint initiatives and projects, Russia and China can create a stable foundation for long-term economic development.

The purpose of this study is to substantiate optimal forms for implementing Sino-Russian technological partnerships in strategically important economic sectors, using the rare earth industry as a case study. The research objectives are as follows:

- to analyze the state of Russia’s rare earth mineral resource base and assess the structure of key Arctic deposits;

- to identify potential sites for international cooperation;

- to compare the consumer markets of Russia and China, as well as development forecasts, in order to identify common features and fundamental differences;

- to develop and compare options for long-term technological cooperation between the two countries in the rare earth industry;

- to determine the most effective forms of cooperation based on the principle of maximum benefits with minimum risks for both parties.

Literature review

Issues related to the development of the mineral resource base, particularly in the Russian Arctic, remain highly relevant in contemporary scientific literature [13-15]. General challenges associated with supplying Russian industry with critical minerals, including REM, are discussed in [16]. It is noted that, in recent years, the mineral resource base of critical metals in Russia has exhibited positive growth, although many complex ore deposits remain undeveloped. According to [17-19], the main obstacles hindering the development of the rare earth industry in Russia include the lack of technologies for separating rare earth oxides and producing metals and alloys, the negative environmental impact of mining and processing, the generally low quality of raw materials, logistical inaccessibility of deposits, especially in the Arctic, high barriers to entering global markets, heavy reliance on imports, limited domestic demand for rare earth metals, insufficient regulatory and industry support mechanisms, the capital-intensive nature of projects, and geopolitical tensions. Nevertheless, several studies [1, 2] indicate promising prospects for the development of the Russian rare earth industry in response to growing domestic and global demand.

The works [20, 21] examine the geological characteristics of specific rare earth deposits in the Murmansk Region, estimate reserve values, provide data on elemental composition, and consider processing technologies, as well as the potential for further development of the rare earth industry in the region. Other studies [22, 23] focus on the development and processing of complex ores at the Tomtor deposit in the Sakha Republic, including data on the granulometric, mineral, and chemical composition of the ores. However, Russian scientific literature still lacks comprehensive approaches for assessing the reserve structure of Arctic rare earth deposits, identifying the most and least abundant elements, and comparing resource availability with market potential, including in the context of increasing exports.

Certain aspects of the development of Chinese rare earth metal deposits are addressed in [7, 24, 25], highlighting issues such as resource depletion and the uneven distribution of heavy and light elements within deposit reserves. Studies examining the development of Russia’s mineral resources sector as a whole [26, 27] note that it currently faces significant global geopolitical and climatic challenges, requiring alternative strategies for industry development.

The issues surrounding the implementation of a Sino-Russian partnership in the rare earth industry have been insufficiently addressed in the scientific literature. Existing studies examine technological cooperation between the two countries in related sectors, such as fuel and energy. For example, the joint Yamal LNG project has provided China with a new trade route and strengthened its role in Arctic infrastructure development, while allowing Russia to attract investment for accelerated regional development and to acquire critical technologies amid tightening European sanctions and the withdrawal of several companies from the Russian market [10]. Another example of successful energy cooperation is the Power of Siberia project, which opens new prospects for ensuring energy security and economic development for both countries [12], while also reinforcing their positions on the global stage and maintaining strategic balance [28]. However, these studies focus mainly on the mutual benefits of cooperation and generally identify risks only for Russia. Moreover, they do not analyze forms of Sino-Russian partnership in strategic sectors from the perspective of optimality for both parties.

The experience of previously implemented initiatives can serve as a basis for refining the forms of Sino-Russian technological partnership in new areas. The scientific hypothesis of this study is as follows: the implementation of a Sino-Russian partnership in the Arctic rare earth industry, based on a comprehensive assessment of reserve structure and market potential, will be optimal and mutually beneficial if it considers the complementarity of resources and technologies and provides specific benefits while minimizing risks for both partners. The scientific novelty of the study lies in its comprehensive assessment of Arctic rare earth metal deposits, review of possible forms of Sino-Russian partnership in the rare earth industry, and the development of optimal partnership models that account for both benefits and risks for the involved parties.

Methods

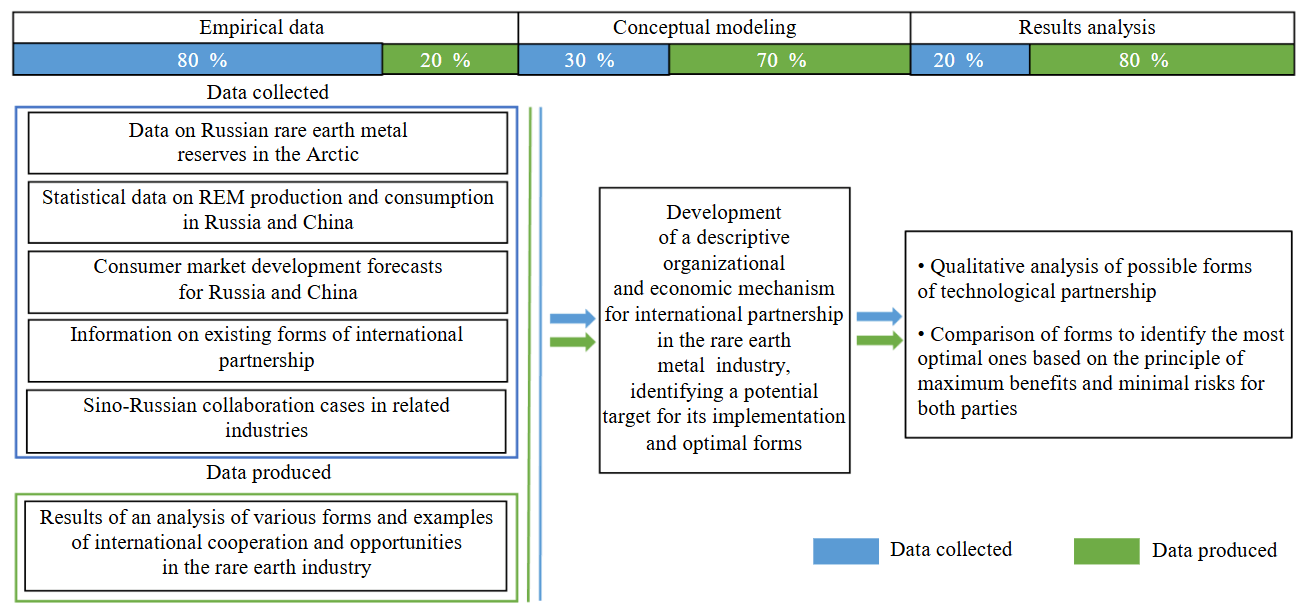

The study employs an empirical-theoretical approach (Fig.1). The research methodology primarily relies on qualitative methods, supplemented by quantitative data. The theoretical framework incorporates the following methods: analysis of relevant scientific literature, general scientific techniques such as analysis, synthesis, comparison, analogy, and conceptual modeling. Comparative ana-lysis serves as a core method throughout the study. It is applied to examine and contrast the structure and volume of rare earth metal reserves at Russian deposits, the production cycles in Russia and China, the composition of consumer demand for rare earth metals in both countries, and various forms and examples of international partnerships. The analogy method is used to draw insights from successful Sino-Russian projects in the fuel and energy sector, such as the Yamal LNG project, the Power of Siberia project, and the joint venture Razrezugol LLC, all of which are implemented in the Russian Arctic. These projects are analyzed and compared based on criteria including process segmentation (investment activities, resource extraction, infrastructure development, provision of equipment and technology, etc.) and the resulting benefits and risks for both parties. Conceptual modeling involves designing a descriptive organizational and economic framework for international partnerships, identifying potential targets for implementation, and developing optimal partnership models based on the principle of maximum benefits and minimum risks.

The primary empirical method employed is statistical analysis, which involves the collection and examination of secondary empirical data from a wide range of sources, including official reserve statistics, industry reports and analytical reviews, regulatory documents, and prior research conducted by the authors.

The object of the study is the rare earth industry, while the subject is the economic and managerial relationships arising from the implementation of a Sino-Russian partnership in the industry, exemplified by the development of Arctic rare earth deposits.

Fig.1. Research methodology

Results and discussion

An analysis of Russian rare earth metal reserves

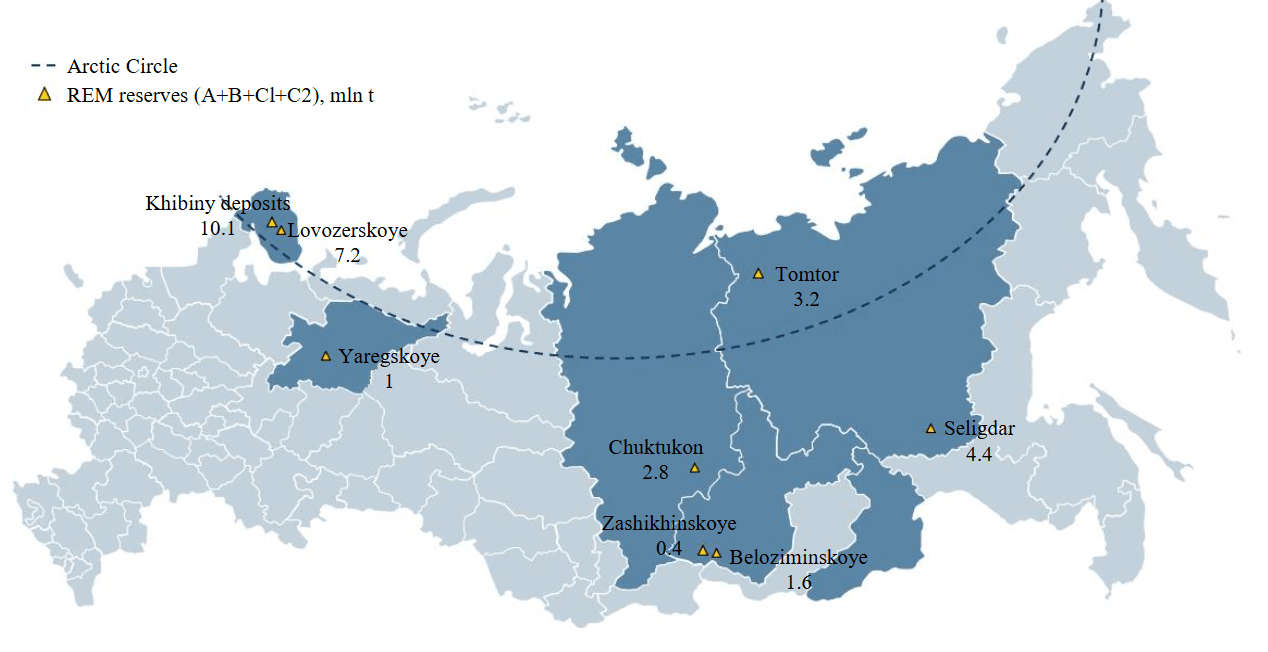

Currently, Russia has approximately ten rare earth metal deposits6, with total reserves of around 30 million t in categories A, B, C1, and C2 (Fig.2). Reserves in categories A, B, and C1 alone amount to roughly 10 million t, positioning Russia as one of the world leaders in rare earth metal reserves (fourth after China, Vietnam, and Brazil)7. Approximately two-thirds of these reserves are concentrated in deposits located in the Russian Arctic, including the Murmansk Region and the Sakha Republic.

Fig.2. Key Russian REM deposits and their reserves

The largest REM reserves are found in deposits within Murmansk Region, such as the Lovozerskoye deposit and the Khibiny group (Kukisvumchorr, Yukspor, Apatitovy Tsirk, Rasvumchorr Plateau, Koashva, Nyorkpahk, and others). Currently, rare earth production in Russia is limited to the Lovozerskoye deposit, which produces approximately 2700 t of metals annually, over 90 % of which are exported as carbonates8. Promising deposits such as Tomtor, Zashikhinskoye, and Yaregskoye are being prepared for development. It is important to note that these deposits are polymetallic and contain other valuable components. For example, the Khibiny deposits primarily produce apatite-nepheline ores and also contains aluminum and titanium reserves. The Yaregskoye deposit is notable as the world’s only source of ultra-high-viscosity oil produced by underground mining and is currently being prepared for the extraction of titanium and other metals, including rare earth elements. The Tomtor and Zashikhinskoye deposits also contain niobium, zirconium, and uranium [18, 19, 22].

Rare earth metals comprise 17 elements from both light and heavy groups. The light group includes lanthanum, cerium, praseodymium, neodymium, promethium, samarium, and europium, while the heavy group includes gadolinium, terbium, dysprosium, holmium, erbium, thulium, ytterbium, lutetium, and yttrium [5]. Scandium is the seventeenth element, which does not belong to either of the two groups.

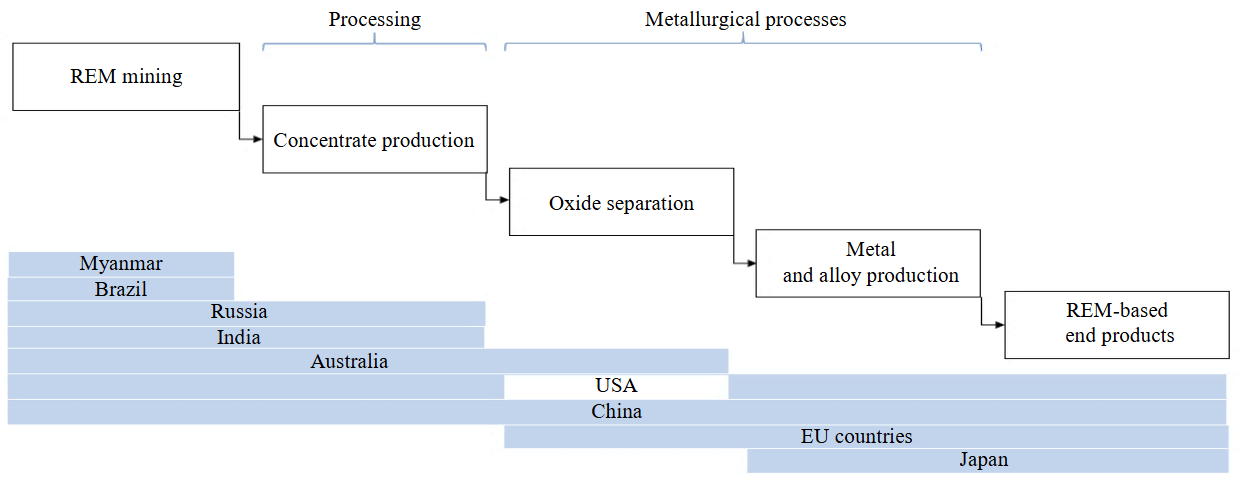

Global REM reserves are commonly calculated by converting them into the sum of their trioxides (∑TR2O3), which can vary significantly in content. For example, the TR2O3 content in the ore of the Tomtor deposit can reach 12 %, one of the highest levels globally, whereas the average content in deposits on the Kola Peninsula does not exceed 1 %8. By comparison, at the world’s largest deposit, Bayan Obo in Inner Mongolia, China (with reserves exceeding 36 million t, more than 80 % of China’s total), the average TR2O3 content is 3-5 %8. In Russia, REM oxides are not produced. The production cycle ends at the production of carbonates obtained from loparite concentrate at Solikamsk Magnesium Plant, which are subsequently exported. The full REM production cycle is illustrated in Fig.3.

In Russia, stages from oxide separation to the production of end products are absent. These stages generate the highest added value. Consequently, Russia exports more REM than it imports in bulk, but imports exceed exports in monetary terms. The main importers of Russian REM are China and EU countries, where metallurgical processing separates REM oxides and produces metals and alloys for high-tech products with significant added value.

Fig.3. Full REM production cycle [20]

The global REM market faces a so-called “balance problem” [5, 17]: an oversupply of light metals and a corresponding shortage of heavy metals, due to the complexity and heterogeneous composition of the ores. Isolating individual elements requires specific separation technologies for each REM. Furthermore, while some metals, such as lanthanum and cerium, are abundant, high-tech industries generate significant demand for heavy elements such as dysprosium and yttrium, and other heavy elements, which are essential for advanced technologies in defense, aviation and aerospace engineering, and other sectors. Consequently, the oversupply of certain REM leads to a decrease in their prices, while scarcity of others drives price increases.

Russian deposits contain reserves of both light and scarce heavy REM, although their composition can vary considerably. Table 1 presents the results of an analysis of the reserve structure of key Arctic deposits: Lovozerskoye (loparite and eudialyte), the Khibiny group, and Tomtor.

Table 1

Light and heavy REM content, thousand t [20, 21, 29, 30]

|

Deposit |

Light REM |

Heavy REM |

||||||||||

|

La |

Ce |

Nd |

Pr |

Sm |

Eu |

Y |

Tb |

Gd |

Dy |

Er |

Yb |

|

|

Lovozerskoye (loparite) |

+9.6 |

+15.7 |

+2.9 |

+0.9 |

– |

– |

– |

– |

– |

– |

– |

– |

|

REM total |

29 |

– |

||||||||||

|

Lovozerskoye (eudialyte) |

+283.1 |

+684.1 |

+330.3 |

+94.4 |

+99.1 |

+22.2 |

+542.6 |

+21.2 |

+59 |

+80.2 |

+47.2 |

+44.8 |

|

REM total |

1 513 |

|

|

795 |

||||||||

|

Khibiny group |

+3058.2 |

+5213.7 |

+1704 |

+462.7 |

+259.6 |

+79 |

+22.6 |

+33.9 |

+214.4 |

+101.6 |

+45.1 |

+45.1 |

|

REM total |

10777.2 |

462.7 |

||||||||||

|

Tomtor |

+754 |

+1380 |

+541 |

+134 |

+80 |

+26 |

+206 |

+8 |

+54 |

+27 |

+18 |

– |

|

REM total |

2915 |

313 |

||||||||||

|

Total by element |

4104.9 |

7293.5 |

2578.2 |

692.2 |

438.7 |

127.2 |

771.2 |

63.1 |

327.4 |

208.8 |

110.3 |

89.9 |

|

REM total |

15234.7 |

1570.7 |

||||||||||

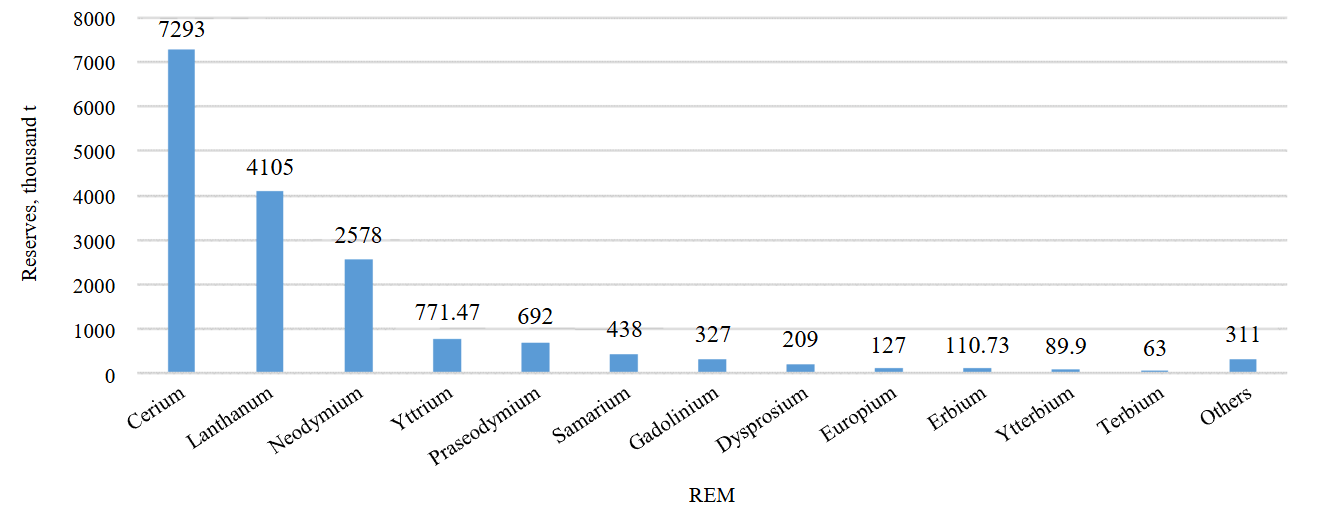

As can be seen from Table 1, the only currently developed deposit, Lovozerskoye (loparite), contains reserves of light REM, such as cerium, lanthanum, neodymium, and praseodymium. These elements are also abundant in the Khibiny group and the Tomtor deposit, which, in addition, contain heavy metals that account for the largest share of their reserves (approximately 10 % of the total). Among the deposits considered, the Khibiny group holds the largest total REM reserves. Total reserves of light metals exceed 10 million t, while heavy metals amount to approximately 460 thousand t; by comparison, the Tomtor deposit, with reserves three times smaller, contains about 310 thousand t of heavy elements. The Tomtor deposit stands out with the highest REM content among the deposits examined, reaching up to 12 %. This represents a significant competitive advantage, as low concentrations of useful components in ore reduce extraction profitability and can render the development of certain reserves economically unfeasible. Figure 4 illustrates the distribution of REM reserves across the examined deposits, ranked from most to least abundant.

Analysis of the reserve structure of the three Arctic deposits indicates that light REM are more abundant than heavy REM. Cerium is the most prevalent element, comprising over 40 % of total reserves. Among heavy elements, gadolinium is the most abundant and terbium the scarcest. The Tomtor deposit in the Sakha Republic stands out due to its significant reserves. The presence of scarce heavy elements, along with unique concentrations of useful components, is expected to boost extraction profitability and improve the KPIs of potential projects. These factors justify selecting this deposit as a potential candidate for certain forms of Sino-Russian technological partnership.

Fig.4. Russian REM reserves by metal

Assessment of rare earth metal applications in industry: comparison of Russian and Chinese consumer markets

The creation of a full production cycle for rare earth metals and their derived products must be supported by corresponding industrial demand. REM are used across a wide range of high-tech sectors, with each element having specific applications. Table 2 summarizes the primary uses of REM.

Table 2

REM applications [31-34]

|

REM |

Application |

|

Lanthanum |

Automotive catalysts, cracking catalysts, metallurgy, hybrid engines, glass industry, polishing powders, batteries, luminophores, optics, lasers, nuclear technology |

|

Cerium |

Automotive catalysts, cracking catalysts, metallurgy, glass industry, polishing powders, batteries, luminophores, textile industry |

|

Praseodymium |

Magnets, automotive catalysts, metallurgy, glass industry, polishing powders, batteries |

|

Neodymium |

Magnets, catalysts, metallurgy, glass industry, batteries, electronics, lasers, hybrid engines |

|

Yttrium |

Luminophores, glass industry, optics, lasers, ceramics, metallurgy, aerospace, nuclear technology |

|

Gadolinium |

Magnets, luminophores, optics, lasers, X-ray technology |

|

Terbium |

Magnets, luminophores, X-ray technology |

|

Dysprosium |

Magnets, catalysts, nuclear power, hybrid engines |

|

Samarium |

Batteries, computers, measuring instruments, magnets |

|

Europium |

Luminophores, nuclear power |

|

Promethium |

Nuclear power, measuring instruments |

|

Holmium |

Glass industry, lasers |

|

Erbium |

Luminophores |

|

Thulium |

X-ray technology |

|

Ytterbium |

Lasers, metallurgy |

|

Lutetium |

Cracking catalysts |

|

Scandium |

Metallurgy, aviation, aerospace engineering, automotive engines |

According to Table 2, lanthanum, cerium, praseodymium, neodymium, and yttrium are in highest demand. Praseodymium and neodymium are particularly important for permanent magnets, which are widely used in wind turbines. Globally, magnet production accounts for roughly 42 % of REM demand9. In China, which is the global leader in wind energy, REM consumption is strongly correlated with the growth of wind power capacity [6]. Several REM are also used in solar photovoltaic devices due to their fluorescent properties10. Accordingly, the green energy sector is expected to drive the most significant growth in REM demand worldwide in the near future.

Lanthanum and cerium are primarily used in catalysts and in battery production, which in turn supports electric vehicles and other forms of transport. Electric vehicle production in China has increased 20-fold over the past decade, driving substantial growth in demand for these metals11. Consequently, global and Chinese demand for REM is closely tied to the expansion of high-tech sectors.

Yttrium, a scarce rare earth element of the heavy group, is used in metallurgy as an alloy additive, for example in high-strength steel and cast iron. While its applications are less widespread than for permanent magnets, the inclusion of yttrium can improve the quality and durability of finished products, particularly in metallurgical applications.

REM consumption in Russia remains limited, with the petrochemical and oil refining sector accounting for roughly 70 %, metallurgy about 10 %, the nuclear industry, and others making up the remainder. Annual consumption is approximately 1.2 thousand t, and this figure has remained largely unchanged12. Previous studies by the authors [6, 31] indicate that medium-term growth in domestic demand will primarily be driven by emerging sectors, such as electric vehicles and green energy, alongside increased usage in traditional industries such as metallurgy and petrochemicals. Forecasts suggest that by 2030, Russian REM consumption could reach 2.3 thousand t, nearly double the current level, with neodymium being the most widely consumed element (Fig.5).

Fig.5. REM consumption in Russia: forecast for 2030 based on [6]

In the medium term, light REM are expected to be the most sought-after in the Russian consumer market. Among these, neodymium, which is used in magnets, batteries, and other high-tech applications, will likely experience the highest demand, followed by lanthanum, which is widely employed in metallurgy, petrochemicals, and oil refining. The projected consumption of heavy REM, including dysprosium, is expected to remain significantly lower than that of light REM. However, heavy metals are used in nuclear power, X-ray imaging, and the military sector. Should growth in these sectors accelerate, total demand for REM in Russia could increase further. Given current and potential future demand, self-sufficiency in domestic reserves would allow Russia to satisfy internal needs over many years while exporting a portion of production with a focus on the Chinese market. In this context, global supply must also continue to meet worldwide demand.

China currently consumes over 170 thousand t of REM annually13, with the largest share (over 40 %) used in the production of magnetic materials. The structure of Chinese REM demand closely mirrors global trends, encompassing metallurgy and instrument manufacturing, petrochemicals and oil refining, ceramics, hydrogen storage materials, luminophores, polishing powders, catalysts, and other sectors. Future growth in Chinese demand will be driven by several key factors14:

- Continuing growth in demand for electric vehicles and other types of transport and their improvement. China’s market for new vehicles is experiencing rapid growth, supported by government policies that sustain high consumer demand. REM are essential in electric vehicles for motors, power steering, and other key components. Lithium batteries and automotive exhaust catalysts also contain REM [35]. Their compact size, light weight, and high performance provide significant advantages, and ongoing technological improvements in both vehicle production and REM materials drive industry growth.

- Advancements in robotics and digital technologies. Robots are used across sectors including automotive, electronics, and household appliances. China has established a full production cycle, from key components to industrial robots and integrated robotic systems. Advances in core technologies, research and development, and mass production capacity continue to expand. In this context, REM are primarily used in robotic server systems and greatly enhance their operational speed.

- Growth in wind energy capacity. China’s carbon neutrality and energy transition policies promote the expansion of wind power [36]. Consequently, demand for REM-based magnets is expected to increase. Recent improvements in semi-direct drive permanent magnet generators, which use less magnetic material than direct-drive systems, may result in lower growth rates of REE magnet demand compared to previous projections.

- Increased production of inverter air conditioners, energy-efficient elevators, and household electronics. New energy efficiency standards have boosted the adoption of high-performance inverter air conditioners, which rely on efficient permanent REM-magnets. REM are also used in energy-saving elevator traction systems, which benefit from their small size, high efficiency, and wear resistance. Neodymium magnets are further applied in speakers, smartphones, wireless headphones, tablets, PC, wearable devices, and wireless chargers. Combined with growth in artificial intelligence and related technologies, this trend is expected to sustain gradual increases in REM demand, particularly for permanent magnet applications.

Overall, REM demand is projected to rise in both Russia and China in the medium term. China seeks to secure additional resources to satisfy growing domestic and global demand, while Russia requires technology and investment to establish closed-loop production cycles. In this context, it is essential to identify strategic sectors where Sino-Russian technological partnerships could be mutually beneficial, including in new, promising regions such as the Arctic. The benefits and risks for each country must be evaluated, and the most optimal forms of collaboration determined, using rare earth production as a case study.

Forms of сooperation between Russia and China in the сontext of the rare earth industry

To identify potential forms of international cooperation, it is necessary to consider the legal framework. Table 3 presents the types of partnerships regulated by relevant legislation, including the Civil Code of the Russian Federation.

Among these, consortia and joint ventures are the most promising forms for the REM industry, as they can facilitate joint deposit development and the creation of processing facilities. Cross-border clusters, which focus on supply chain integration, may become relevant in later stages of cooperation, provided that relevant companies exist in the bordering regions. Other forms, such as research consortia and special investment contracts, primarily support technological development and infrastructure construction, which have already been applied in Russia. One of the key conditions for cooperation in the REM sector, however, is that it must be optimal for and bring benefits to both parties.

Table 3

Forms of international cooperation15

|

Cooperation form |

Participants |

Validity period |

Features |

Application potential in the REM industry |

|

Consortium |

Temporary merger of companies without forming a legal entity |

Project deadline |

Flexible structure, contractual liability, no need to create a legal entity |

Establishment of processing industries, joint development of deposits |

|

Joint venture |

Russian and international legal entities and indivi-duals |

Indefinitely (according to the charter) |

Restrictions regarding strategic industries, the possibility of government control; the need to create a legal entity |

Establishment of processing industries, joint development of deposits |

|

Concession agreementwithinternational participation |

The government and international investors |

Established by agreement |

The investor receives the right to operate the facility (usually infrastructure), whereas the government retains ownership |

Infrastructure development |

|

Special investment contract (SPIC) |

The government and Russian/international investors |

Up to 15-20 years (validity period may be extended) |

Mandatory localization: prefe-rential terms are provided to investors in exchange for loca-lization of production |

Establishment of high-tech REM-based production, development of new technologies |

|

Research consortium |

Research organizations, universities, corporations |

3-10 years on average |

Joint research and development activities, the possibility of receiving government support, joint use of results |

Development of technologies for the extraction and processing of rare earth metals, creation of new materials |

|

Cross-border clusters |

Businesses operating in bordering regions |

Long term |

Association of businesses opera-ting in bordering regions, production cycles coordination, special economic regimes |

Establishment of logistics chains for rare earth metals |

As for concession agreements, they are typically used in infrastructure projects. A notable example of this type of cooperation between Russia and China is the Amur River bridge project16.

Currently, there are no examples of Sino-Russian cooperation in REM extraction and processing. Unlike other strategic sectors, such as energy, the REM industry remains largely untapped in terms of Sino-Russian partnership potential (Table 4).

One of the most well-known examples of successful cooperation is the Yamal LNG project. Implemented in the Yamalo-Nenets Autonomous Region, the project’s investors include Novatek (Russia), CNPC (China), and the Silk Road Fund. Its significance for Russia lies not only in gaining access to technologies adapted to harsh Arctic conditions but also in providing a route to Asian markets amid restricted access to Western resources [10]. Within the project, China contributed financing (both direct and credit investments), technology, and equipment, including LNG tankers, gas liquefaction modules. For China, the project provided increased energy supplies, a new trade route, and a stronger position in Arctic infrastructure development.

Another example is the Power of Siberia gas pipeline project, which serves as a channel for Russian gas supplies to China and other Asian countries while linking Russia’s domestic gas transportation systems. The project was designed to reduce Russia’s dependence on European gas markets amid geopolitical tensions and to access rapidly growing Asian markets. For China, it represents a new energy source that complements domestic production and is cheaper than LNG delivered by tankers. The benefits are mutual: for China, the project expands influence in Russian energy markets, mitigates energy risks from the United States and allies, supports internationalization of the yuan, and reduces legal risks via investment in Russia [12]. For Russia, the pipeline guarantees sales, generates revenue, and creates jobs. However, reliance solely on raw materials cooperation poses a risk to Russia’s manufacturing industry. Moreover, China maintains long-term contracts for pipeline gas from Kazakhstan, Uzbekistan, and Turkmenistan (the latter alone accounted for 50 % of China’s natural gas imports in 202317) and is pursuing new agreements with Qatar, Australia, and other suppliers, which may limit Russia’s market share despite potential increases in supply.

These examples illustrate the consortium model, which is the most common form of international partnership. A joint venture represents a more complex mechanism. Examples of such coope-ration between Russia and China include Razrezugol LLC, a joint venture established by Russia's energy company En+ and China's CHN Energy. The project involves the construction of infrastructure for a coal deposit in Zabaikalsky Krai, which is currently underway. The deposit is expected to reach its full design capacity by the end of 202718; however, the project is already facing financing difficulties related to sanction-induced restrictions on international payments. Another example of a joint venture is Sakhalin Energy LLC, which, although not a Sino-Russian partnership, previously served as the operator of the Sakhalin-2 oil and gas development project. At the time of its establishment, three international companies (Shell, Mitsui, and Mitsubishi) were shareholders, and operations were conducted under a Production Sharing Agreement with the Russian Federation. In 2007, Gazprom became a shareholder. In 2022, however, international partners withdrew from the project due to geopolitical factors. As a result, the original company was r eplaced by the Russian entity

Table 4

|

Cooperation form |

Implementation |

Process segmentation |

Benefits |

Risks |

||

|

For Russia |

For China |

For Russia |

For China |

|||

|

|

|

|

|

|

|

|

|

Consortium |

Yamal LNG |

Capital investment (direct and credit financing): Russia, China, France (early stages). Infrastructure development: Russia, China. Technology provision: China, Russia. Resource extraction: Russia. Processing: Russia, China |

• Attracting investment and resources for the development of the Arctic. • Supply of imported technologies and equipment. • Creation of new jobs in the region |

• New sources of energy supplies. • New trade routes for the export of energy resources and other goods. • Expanding influence in the Arctic Region

|

• Environmental risks asso-ciated with the need to comply with more stringent environmental requirements in the region. • Risks associated with the unstable LNG pricing system. • Technological risks, such as the risk of restrictions on project modernization and digitalization due to sanctions, and increased dependence on Chinese technology and equipment |

• In addition to environmental risks, there is additional reputational liability, as well as the necessity to comply with Russian legislation. • Currency risks due to high ruble volatility. • Dependence on Russian infrastructure, including nuclear icebreakers. • Political and sanctions risks. • Changes in Russian tax legislation. • Dependence on long-term contracts; limited flexibility in the face of market fluctuations |

|

Power of Siberia |

Capital investment: Russia (China signed a 30-year sales agreement worth 400 USD billion). Infrastructure development: Russia (partially China). Technology provision: Russia. Resource extraction: Russia. Processing: China, Russia |

• Access to fast-growing Asian energy markets. • New reliable distribution channels. • Creation of new jobs in the underdeveloped Far East Region. • Expansion of Russia's gas transportation system |

• New sources of relatively inexpensive energy supplies and the associated reduction in energy dependence risks. • Long-term (30-year) contracts for resource supplies. • Supplier diversification. • Obtaining preferential pri-cing conditions among buyers of Russian gas. • Reduction in logistics costs. • Creation of infrastructure for future projects (Power of Siberia-2) |

• The stagnation of processing technology development and the lack of high-value-added production in Russia create technological risks. • The raw material supply sector is sensitive to geopolitical fluctuations. • Limited opportunities for expanding cooperation as a result of China’s diversification of raw material supply sources. • Risks to fragile ecosystems associated with infrastructure development (pipelines, roads) |

• Geopolitical tensions introduce uncertainty into new contracts. • Dependence on Russian infrastructure. • Sanctions pressure due to cooperation with Gazprom. • Risk of supply disruptions due to pipeline accidents |

|

|

Joint venture |

Razrezugol LLC |

Capital investment: Russia, China. Infrastructure development: Russia, China. Technology provision: Russia, China. Resource extraction: Russia, China |

• Receiving financial investment from CHN Energy in resource development and infrastructure. • Infrastructure development, improving transport and energy logistics in the region through the construction of roads, a railway station, and energy sector facilities. • Creation of jobs. • Increased export potential; diversification of coal markets. • Use of Chinese technologies in coal mining and logistics |

• Guaranteed coal supplies and long-term access to Russian energy resources. • Reduced dependence on other suppliers. • Logistics savings due to the deposit’s proximity to the Chinese border. • Strengthening CHN Energy's position in the Russian coal industry, opening up opportunities for new projects |

• Funding issues due to sanctions. • There is a risk of foreign partners leaving, which will require a company reorga-nization (similar to Sakhalin Energy). • Potential limitations in equipment maintenance or spare parts supplies. • Growth in coal mining may lead to environmental pollution, protests by local residents, and stricter regulations. • High influence of global market conditions on coal sales |

• Tighter regulation or natio-nalization of assets may impact investment returns. • Sanctions against Russia may complicate coal transportation (e.g., restrictions on maritime shipping). • Tighter regulation in the coal industry may require additional investment in environmental measures. • In the long term, tightening climate policies both in China and globally may lead to a decrease in coal demand |

Sakhalin Energy LLC19. The reviewed forms of Sino-Russian partnership, along with their associated benefits and risks, are summarized in Table 4.

Among the forms of technological cooperation considered, a consortium-based joint project appears to be the most optimal option for both Russia and China. This format allows Russia to attract investment, advanced technologies, and equipment required for Arctic development, while providing China with access to new sources of raw materials. Such cooperation is expected to yield long-term benefits for both parties: upon completion of the project, Russia will retain the technologies necessary to establish full production cycles in the rare earth industry, while China will secure new strategic trade routes, particularly via the Northern Sea Route, and strengthen its presence in the Arctic Region. Compared with other forms of cooperation, such as joint ventures, a consortium is a more flexible arrangement implemented within a defined timeframe, which helps mitigate pricing, market, and long-term geopolitical risks. Moreover, joint ventures require the establishment of a legal entity, creating additional risks for Russia: in the event of a partner’s withdrawal, the company must undergo rapid restructuring. For China, participation in a joint venture must be justified not only by current demand but also by long-term strategic needs, which are inherently difficult to forecast. Overall, the risks associated with consortium-based cooperation are significantly lower than those of joint ventures, which, as past experience demonstrates, are more vulnerable to shifts in market conditions, geopolitical dynamics, and other conditions due to their organizational and economic features.

Conclusion

Russia currently lags behind China, which has established full production cycles for rare-earth metal products used in electronics, robotics, electric vehicle, renewable energy, and other industries. In Russia, these sectors are either underdeveloped or at an early stage of formation. However, the development of the mineral resource base represents a key area where the strategic interests of Russia and China converge. The Arctic Region possesses substantial potential for the development of its mineral resources and the expansion of new trade routes, making it an area of growing interest for multiple nations. The unique reserves of the Tomtor deposit could serve as a foundation for the advancement of Sino-Russian cooperation in the Arctic. Russia’s resource potential enables it to meet both domestic and international demand, which is of particular interest to China amid sustained growth in global REM consumption.

This study of Sino-Russian partnership in the Arctic, using the REM industry as a case study, has yielded results with both scientific and practical relevance for strategic economic sectors. Among the cooperation models examined, a consortium-based partnership, similar to the Yamal LNG and Power of Siberia projects, emerges as the most promising. This format allows Russia to attract investment and technology, while enabling China to secure access to new sources of raw materials and enhance its strategic position in the Arctic. Alternative formats, such as joint ventures, are less advantageous for Russia and entail additional risks for China. Other forms of cooperation, including research consortia, cross-border clusters, and concession agreements, are not optimal at the current stage for either of the two parties but may be applied at later phases of technological partnership.

The findings of this research may be used at the national level to inform strategies for the deve-lopment of the REM industry and other strategic segments of the mineral resources sector, strengthen international cooperation between Russia and China, and support businesses planning investment projects in the Arctic, including mineral resource development and the establishment of full production cycles. Future research may focus on strengthening the economic and geopolitical dimensions of the analysis, particularly by examining the impact of international sanctions and trade restrictions on Sino-Russian cooperation, as well as exploring opportunities to diversify REM export markets, including countries in Asia and the Middle East. Additional research may also assess Arctic infrastructure projects, identifying opportunities for logistics optimization and cost reduction in order to generate both qualitative and quantitative insights.

Overall, Sino-Russian partnership in the Arctic has significant potential to strengthen the global positions of both countries in the REM market. The successful implementation of joint projects, including the development of Arctic deposits, could become a key driver of technological and economic growth. However, achieving maximum impact requires careful consideration not only of economic benefits, but also of environmental, social, and geopolitical risks. Continued research in this area will contribute to a deeper understanding of the opportunities and challenges associated with Arctic resource development.

State Report on the Status and Use of Russian Mineral Resources in 2023. Moscow: Rosnedra, 2024, p. 710 (in Russian).

Zhiyan Consulting: Analytical Report on the Current Performance and Development Trends in the Chinese Rare Earth Industry in 2023 (in Chinese). URL: www.chyxx.com/industry/1137248 (accessed 28.04.2025).

Mineral Commodity Summaries 2024. U.S. Geological Survey, 2024, p. 212. DOI: 10.3133/mcs2024

Huibo Smart Investment Research: In-Depth Analysis of the Rare Earth Industry: Supply-Demand Balance and Market Landscape (in Chinese). URL: hibor.com.cn/data/ec51894e6abe55ca5187ab4bf54bd162 (accessed 28.04.2025).

State Report on the Status and Use of Russian Mineral Resources in 2023. Moscow: Rosnedra, 2024, p. 710 (in Russian).

State Report on the Status and Use of Russian Mineral Resources in 2023. Moscow: Rosnedra, 2024, p. 710. (in Russian).

U.S. Geological Survey: Mineral Commodity Summaries 2024. URL: pubs.usgs.gov/publication/mcs2024 (аccessed 01.03.2025).

State Report on the Status and Use of Russian Mineral Resources in 2023. Moscow: Rosnedra, 2024, p. 710 (in Russian).

Demand for rare earth oxides worldwide in 2019 and 2025 by end use. URL: statista.com/statistics/449722/rare-earth-estimated-demand-globally-by-application (accessed 16.09.2025).

Zhiyan Consulting: Analytical Report on the Current Performance and Development Trends in the Chinese Rare Earth Industry in 2023 (in Chinese). URL: chyxx.com/research/yejin/list_6 (accessed 28.04.2025).

Electric vehicles – China. URL: statista.com/outlook/mmo/electric-vehicles/china#unit-sales (accessed 16.09.2025).

State Report on the Status and Use of Russian Mineral Resources in 2023. Moscow: Rosnedra, 2024, p. 710 (in Russian).

Zhiyan Consulting: Analytical Report on the Current Performance and Development Trends in the Chinese Rare Earth Industry in 2023 (in Chinese). URL: chyxx.com/research/yejin/list_6 (accessed 28.04.2025).

Huibo Smart Investment Research: In-Depth Analysis of the Rare Earth Industry: Supply–Demand Balance and Market Landscape (in Chinese). URL: hibor.com.cn/data/ec51894e6abe55ca5187ab4bf54bd162 (accessed 28.04.2025).

Civil Code of the Russian Federation (Part One) N 51-FZ of November 30, 1994 (as amended on July 29, 2017); Federal Law N 115-FZ “On Concession Agreements” of July 21, 2005 (as amended on November 30, 2024); Federal Law N 160-FZ “On Foreign Investments in the Russian Federation” of July 9, 1999.

Construction of the first cross-border road bridge across the Amur River between the Russian Federation and China (Blagoveshchensk – Heihe) (in Russian). URL: btsmost.ru/object/blagoveshensk (accessed 16.09.2025).

Energy Institute: Statistical Review of World Energy 2024. URL: connaissancedesenergies.org (accessed 18.06.2025).

En+ is investing approximately 50 billion rubles in the largest coal project in Transbaikalia. URL: enplusgroup.com/ru/media/news/press/en-investiruet-poryadka-50-mlrd-rubley-v-krupneyshiy-ugolnyy-proekt-zabaykalya (accessed 16.09.2025).

Sakhalin Energy. Company Profile. Overview. URL: sakhalinenergy.ru/ru/company/overview (accessed 16.09.2025).

References

- Kryukov V.A., Yatsenko V.A., Kryukov Ya.V. The REM-Energy Transition Interrelation in the Context of Full-Cycle Projects. Geology of Ore Deposits. 2023. Vol. 65. N 5, p. 416-427. DOI: 10.1134/S1075701523050057

- Yatsenko V.A., Lebedeva M.E. Demand Forecasting in World Rare Earth Metals Market. World of Economics and Management. 2021. Vol. 21. N 4, p. 124-145 (in Russian). DOI: 10.25205/2542-0429-2021-21-4-124-145

- Mikhailov A.V., Bouguebrine C., Shibanov D.A., Bessonov A.E. Impact Evaluation of Excavator Positioning on Open Pit Slope Stability. International Journal of Engineering, Transactions A: Basics. 2025. Vol. 38. Iss. 1, p. 99-107. DOI: 10.5829/ije.2025.38.01a.10

- Petrov I.M., Belousova E.V., Petrova A.I. The development of renewable energy and environmentally friendly transport – the main directions of growth in global demand for high-tech rare metals. Prospect and protection of mineral resources. 2020. N 3, p. 53-56 (in Russian).

- Kryukov V.A., Yatsenko V.A., Kryukov Ya.V. Rare Earth Industry – How to Take Advantage of Opportunities. Russian Mining Industry. 2020. N 5, p. 68-84. DOI: 10.30686/1609-9192-2020-5-68-84

- Cherepovitsyn A.E., Dorozhkina I.P., Soloveva V.M. Forecasts of Rare-earth Elements Consumption in Russia: Basic and Emerging Industries. Studies on Russian Economic Development. 2024. Vol. 35. N 5, p. 688-696. DOI: 10.1134/S1075700724700229

- Xingli Jia, Bo Zhang, Zhongshuai Jia et al. Recovery of niobium, titanium and rare earths from Bayan Obo tailings via silicothermic reduction and targeted crystallization. Minerals Engineering. 2025. Vol. 234. N 109718. DOI: 10.1016/j.mineng.2025.109718

- Jihye Kim, Junhyun Choi, Sugyeong Lee. A Review of Rare Earth Elements Recovery from Bastnaesite Ore: From Beneficiation to Metallurgical Processing. Journal of Sustainable Metallurgy. 2025. Vol. 11, p. 773-798. DOI: 10.1007/s40831-025-01019-0

- Niam A.C., Ya-Fen Wang, Shyh-Wei Chen, Sheng-Jie You. Recovery of rare earth elements from waste permanent magnet (WPMs) via selective leaching using the Taguchi method. Journal of the Taiwan Institute of Chemical Engineers. 2019. Vol. 97, p. 137-145. DOI: 10.1016/j.jtice.2019.01.006

- Afanasev S.N., Fadeev A.M. Sino-Russian technological partnership in the Arctic on the example of Yamal LNG project. Arctic and Innovations. 2025. Vol. 3. N 1, p. 33-41 (in Russian). DOI: 10.21443/3034-1434-2025-3-1-33-41

- Iakhiaev D., Grigorishchin A., Zaikov K. et al. Methodological approach to assessing the digital infrastructure of the northern regions of the Russian Federation. Journal of Infrastructure, Policy and Development. 2024. Vol. 8. Iss. 12. N 8747. DOI: 10.24294/jipd.v8i12.8747

- Zemtsov A.S. Benefits and risks for Russia and China from the interconnection of energy infrastructure. Bulletin of Moscow Witte University. Series 1: Economics and Management. 2024. N 2 (49), p. 80-88 (in Russian). DOI: 10.21777/2587-554X-2024-2-80-88

- Nevskaya M., Shabalova A., Nikolaichuk L., Kirsanova N. Development of a Quantitative Assessment Algorithm for Operational Risks in Mining Engineering. Resources. 2025. Vol. 14. Iss. 4. N 53. DOI: 10.3390/resources14040053

- Semenova T., Sokolov I. Theoretical Substantiation of Risk Assessment Directions in the Development of Fields with Hard-to-Recover Hydrocarbon Reserves. Resources. 2025. Vol. 14. Iss. 4. N 64. DOI: 10.3390/resources14040064

- Dmitrieva D., Solovyova V. Russian Arctic Mineral Resources Sustainable Development in the Context of Energy Transition, ESG Agenda and Geopolitical Tensions. Energies. 2023. Vol. 16. Iss. 13. N 5145. DOI: 10.3390/en16135145

- Bortnikov N.S., Volkov A.V., Galyamov A.L. et al. Fundamental Problems of Development of the Mineral-Resource Base of High-Tech Industry and Energy of Russia. Geology of Ore Deposits. 2022. Vol. 64. N 6, p. 313-328. DOI: 10.1134/S1075701522060022

- Bryantseva O.S. The state and development opportunities of the Russian rare earth industry in the context of the fourth industrial revolution. Russian Economic Bulletin. 2022. Vol. 5. N 6, p. 264-271 (in Russian).

- Maksimova V.V., Krasavtseva E.A., Savchenko Ye.E. et al. Study of the composition and properties of the beneficiation tailings of currently produced loparite ores. Journal of Mining Institute. 2022. Vol. 256, p. 642-650. DOI: 10.31897/PMI.2022.88

- Ponomareva M.A., Cheremisina O.V., Mashukova Yu.A., Lukyantseva E.S. Increasing the efficiency of rare earth metal recovery from technological solutions during processing of apatite raw materials. Journal of Mining Institute. 2021. Vol. 252, p. 918-927. DOI: 10.31897/PMI.2021.6.13

- Kalashnikov A.O., Konopleva N.G., Danilin K.P. Rare earths of the Murmansk Region, NW Russia: Minerals, extraction technologies and value. Applied Earth Science: Transactions of the Institutions of Mining and Metallurgy. 2023. Vol. 132. Iss. 1, p. 52-61. DOI: 10.1080/25726838.2022.2153000

- Kalashnikov A.O., Konopleva N.G., Pakhomovsky Ya.A., Ivanyuk G.Yu. Rare Earth Deposits of the Murmansk Region, Russia – A Review. Economic Geology. 2016. Vol. 111. N 7, p. 1529-1559. DOI: 10.2113/econgeo.111.7.1529

- Malkova M.Yu., Zadiranov A.N., Zaya Kyaw, Dkhar P. Ore of the Tomtor rare-earth deposit for its industrial processing. Journal of Physics: Conference Series. 2020. Vol. 1687. N 012038. DOI: 10.1088/1742-6596/1687/1/012038

- Matveev A.I., Tolstov A.V., Petrov I.M. The proposal for developing a rare metal cluster in the Republic of Sakha (Yakutia). Arctic and Subarctic Natural Resources. 2025. Vol. 30. N 1, p. 7-27 (in Russian). DOI: 10.31242/2618-9712-2025-30-1-7-27

- Houjian Li, Yanjiao Li, Fangyuan Luo, Lili Guo. Navigating extreme risk spillovers: Building a synergistic network of rare earths, green bonds, and clean energy markets in China. Energy Economics. 2025. Vol. 147. N 108562. DOI: 10.1016/j.eneco.2025.108562

- Tian-Yu Zhao, Wei-Lun Li, Kelebek S. et al. A comprehensive review on rare earth elements: resources, technologies, applications, and prospects. Rare Metals. 2025. Vol. 44. Iss. 10, p. 7011-7040. DOI: 10.1007/s12598-025-03459-9

- Jingna Kou, Fengjun Sun, Wei Li, Jie Jin. Could China Declare a “Coal Phase-Out”? An Evolutionary Game and Empirical Analysis Involving the Government, Enterprises, and the Public. Energies. 2022. Vol. 15. Iss. 2. N 531. DOI: 10.3390/en15020531

- Galevskiy S., Haidong Qian. Developing and validating comprehensive indicators to evaluate the economic efficiency of hydrogen energy investments. Operational Research in Engineering Sciences: Theory and Applications. 2024. Vol. 7. Iss. 3, p. 188-207. DOI: 10.5281/zenodo.15093154

- Savostova T.L., Biryukov A.L. Institutional mechanisms for the strategic partnership between Russia and China: the innovative integration. Russian Journal of Industrial Economics. 2016. N 2, p. 108-115 (in Russian). DOI: 10.1707/2072-1663-2016-2-108-115

- Lalomov A.V., Grigoreva A.V. Mineralogy of rare-metal pacer deposits of the Lovozero massif. Trudy Fersmanovskoi nauchnoi sessii GI KNTs RAN. 2022. N 19, p. 190-194 (in Russian). DOI: 10.31241/FNS.2022.19.035

- Kalashnikov A.O., Konopleva N.G., Ivanyuk G.Yu. Valuation of rare earth elements in ore deposits in the Murmansk Region. Gornyi zhurnal. 2020. N 9, p. 42-46 (in Russian). DOI: 10.17580/gzh.2020.09.05

- Cherepovitsyn A.E., Dorozhkina I.P., Guseva T.V., Burvikova Yu.N. Problems and institutional framework for the development of the rare earth metals industry in Russia. Tsvetnye metally. 2024. N 8, p. 58-69 (in Russian). DOI: 10.17580/tsm.2024.08.09

- Marinina O.A., Ilyushin Y.V., Kildiushov E.V. Comprehensive Analysis and Forecasting of Indicators of Sustainable Development of Nuclear Industry Enterprises. International Journal of Engineering, Transactions B: Applications. 2025. Vol. 38. Iss. 11, p. 2527-2536. DOI: 10.5829/ije.2025.38.11b.05

- Cheremisina O.V., Balandinsky D.A., Gorbacheva A.A. et al. Physicochemical features of action of ethoxylated esters of phosphoric acid with different degree of ethoxylation in conditions of froth flotation of apatite. Colloids and Surfaces A: Physicochemical and Engineering Aspects. 2025. Vol. 708. N 135974. DOI: 10.1016/j.colsurfa.2024.135974

- Yujra Rivas E., Vyacheslavov A., Gogolinskiy K.V. et al. Deformation Monitoring Systems for Hydroturbine Head-Cover Fastening Bolts in Hydroelectric Power Plants. Sensors. 2025. Vol. 25. Iss. 8. N 2548. DOI: 10.3390/s25082548

- Shiyue Zheng, Xiaoyong Zhu, Zixuan Xiang et al. Technology trends, challenges, and opportunities of reduced-rare-earth PM motor for modern electric vehicles. Green Energy and Intelligent Transportation. 2022. Vol. 1. Iss. 1. N 100012. DOI: 10.1016/j.geits.2022.100012

- Lisha Tang, Pervukhin D.A. Enhancing operational efficiency in coal enterprises through capacity layout optimisation: A cost-effectiveness analysis. Operational Research in Engineering Sciences: Theory and Applications. 2024. Vol. 7. Iss. 3, p. 144-167. DOI: 10.5281/zenodo.15093139